In the battle for relevance between traditional financial institutions and fintech disruptors, the best ally for the old-guard is turning out to be, unsurprisingly, fintech. Cognitive technology companies like IBM and Coseer are helping Banks, Wealth Managers, Insurance companies and other financial enterprises win against new-age technology driven fintech startups.

Detractors point out, very rightly so, to the difference in experiences for a common task like sending a friend $100. With a Paypal or Square Pay, you just take a snap of your card, type out your friend’s phone number and you are done. With a Bank, you may have to fill up forms, pay $35 and wait for 3-5 days. There are similar stories in each aspect of finance – lending, investing, plan administration, etc.

It’s not that the banks hate consumers. On the contrary. If they could afford it, they would rather have a personal teller who would speak to you in natural language, clarify what you mean, leverage on your personal history and complete the task right away. If they could afford it, they would have a team to anticipate your every need, and advise you at every step with sound options.

It turns out, for the first time in the history of banking, now they can finally afford it. Thanks to technologies like Watson and Coseer, the traditional financial institutions are redefining both, their consumer product and the consumer experience. They are being more intelligent, more personalized, and more human by being more automated. Combined with their millions of long-standing trust-based relationships, this puts the traditional financial enterprises in an enviable position. For example, when Charles Schwab launched its Robo-Advisor, within months the assets under management overtook the Silicon Valley favorites like Wealth Front and Betterment that have been around for years.

Traditional financial firms are being more intelligent, more personalized, and more human by being more automated.

As always, in truth the story unfolds not by a magician’s sweep and pixie dust, but through a series of blocking and tackling steps. Cognitive technology is being applied to multiple facets of a financial enterprise. For example, cognitive computers are beginning to interact with customers, giving them better, quicker answers. Or, in the back office qualitative information esp. social, is being folded in with quantitative information for far superior risk analytics. Or, finance professionals are becoming disruptively productive using the idea of artificial interns.

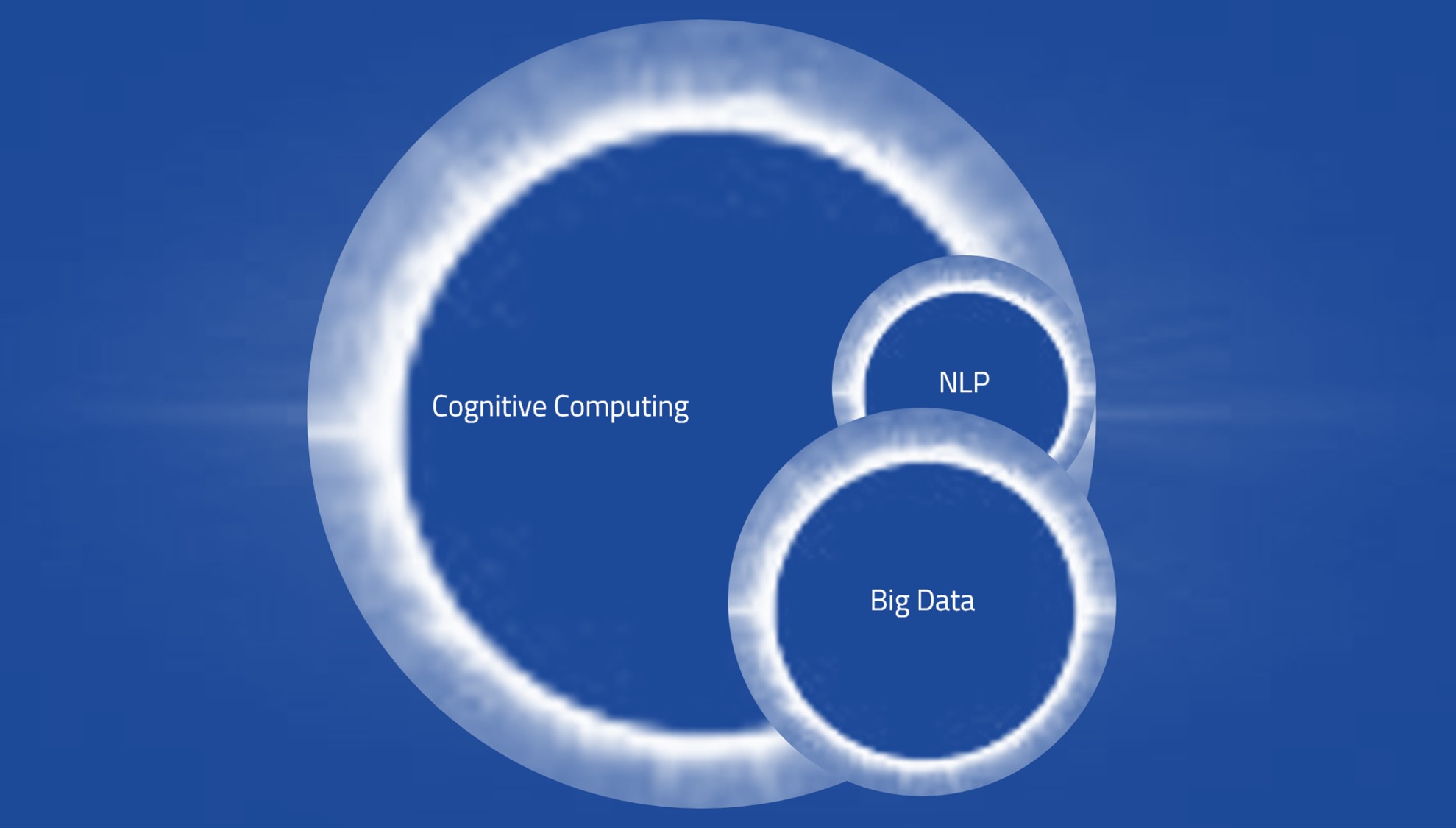

Two distinct models are emerging in the nascent market of cognitive computing. IBM’s Watson takes an investment of time and money worthy of a super computer, but then combines text, speech, visual signals and others to solve foundational challenges. Tactical cognitive computing companies may have a light foot print, but go after specific problems to achieve high accuracy within weeks. For example, startup Coseer focuses on language only and scales language driven workflows. Or Sentient focuses on images.

Traditional firms win because they have the data, the customers trust, and thanks to Cognitive Computing, and endless pool of resources to experiment.

Surprisingly, both models are beating fintech at its own game. The general purpose nature and adaptability of these technologies are letting financial enterprises emulate a fintech starup very quickly, with or without big budgets. Then they have all the data, the life blood of any modern technology and the relationships, the soul of any business.

In this battle of Fintech vs Fintech, it is too soon to write off the old guard.